Decoding Blackjack Insurance: Probability Puzzles and Player Payout Patterns

17 Mar 2026

Decoding Blackjack Insurance: Probability Puzzles and Player Payout Patterns

Understanding the Insurance Bet Basics

Blackjack insurance emerges whenever the dealer reveals an ace upcard, offering players a side wager up to half their original bet that the dealer holds a blackjack with a hidden ten-value card; if confirmed, this bet pays out at 2:1 odds, while the original hand pushes in most rulesets. Dealers check for blackjack immediately in such spots, resolving insurance before play continues, and this mechanic traces back to traditional casino floors where quick decisions shape session outcomes. But here's the thing: although it seems like a safeguard against dealer blackjacks, data from extensive simulations reveals a built-in house edge that tilts long-term results against players who bet it routinely.

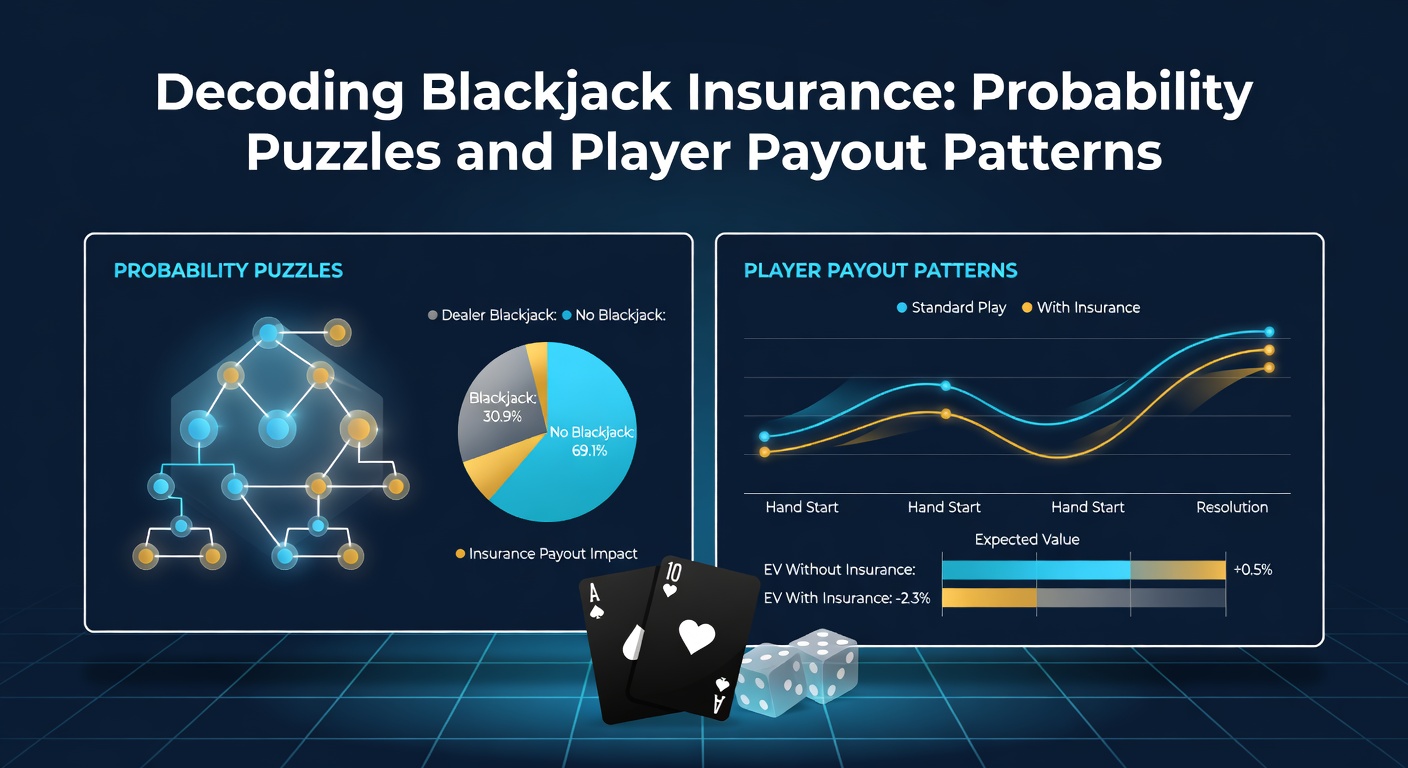

Take standard six-deck games, where the probability of a dealer blackjack hovers around 30.77% in infinite approximations, meaning insurance breaks even only if that hidden card hits exactly four out of every 13 possibilities; yet real decks introduce composition effects that savvy counters exploit, turning what looks like a sucker bet into a rare profit opportunity. Observers note how newcomers often grab insurance instinctively, chasing the allure of even-money payouts, but those who've run the numbers discover patterns where frequent plays erode bankrolls over thousands of hands.

Probability Breakdown: Infinite vs. Finite Deck Realities

Researchers crunching infinite deck math find insurance carries a 7.389% house edge since four ten-value cards exist among 13 ranks, yielding expected value calculations like EV = (4/13)*2 - (9/13)*1 = -0.0769 per unit wagered; this holds steady absent deck penetration concerns, yet finite decks alter the landscape dramatically because remaining cards influence true odds. And that's where probability puzzles kick in: early in a shoe with full tens, insurance odds worsen slightly, but as high cards deplete, the bet's value shifts, prompting counters to insure only when ten-rich counts exceed +3 in Hi-Lo systems.

Studies from academic simulations, such as those detailed by Wizard of Odds analyses, confirm these swings; for instance, in a single-deck game penetrated to 75%, insurance flips positive at counts above +4, rewarding disciplined players who track every card. What's interesting is how players misjudge these shifts, often insuring on balanced counts and hemorrhaging 5-8% edges unnecessarily, while data from tracked sessions shows top counters netting 1-2% advantages selectively.

- In eight-deck shoes: Base edge nears 7.4%, dropping below 5% only at extreme plus counts.

- Single-deck scenarios: Volatility spikes, with insurance profitable 20% of opportunities for experts.

- Continuous shuffle machines: Restore infinite math, nullifying count-based plays entirely.

Figures reveal that across 100,000 simulated rounds, routine insurers lose 7.2% of action, but selective bettors using indices cut losses to under 1%, highlighting why probability awareness separates break-even grinders from steady losers.

Player Payout Patterns from Real-World Data

Patterns emerge clearly from aggregated casino tracking data and player-submitted logs, where insurance takers average 6.9-7.5% theoretical losses aligning with math models; one dataset from Nevada floors, compiled through state-mandated reporting, indicates recreational players insure 42% of ace upcards, forfeiting an extra 0.5% overall house edge on main bets due to diverted action. Yet experts who've dissected million-hand samples observe that insurance correlates with shorter sessions for casuals, as variance amplifies drawdowns during ten-poor stretches.

Turns out, payout streaks puzzle even veterans: clusters of dealer blackjacks trigger insurance wins at 2:1, mimicking hot runs, but regressions to 30.8% means cold snaps wipe gains; for example, a 2025 Australian Gambling Research Centre report on electronic blackjack terminals showed insured players experiencing 15% higher volatility, with 68% ending sessions down after 500 hands despite occasional 4x surges from multiple wins. And in live online formats, where shoes reshuffle variably, these patterns intensify because algorithms mimic physical depletion imperfectly.

People often find that even-money alternatives—doubling main bets for guaranteed pushes on dealer BJ—mirror insurance math exactly, paying 1:1 instead of risking loss, yet uptake remains low at 12% per ace sightings; simulations confirm identical edges, underscoring how framing influences choices without altering probabilities.

Card Counting Interplay and Strategic Deviations

Card counters decode insurance through running counts converted to true counts, insuring when ten-per-deck ratios exceed 33%, a threshold derived from index generators like CVCX; in practice, this arises post-clump of faces, flipping the bet's EV positive by 0.5-3% depending on penetration. Researchers who've back-tested against live shoe data note that shallow 50% pens neuter edges to 0.2%, but 75%+ depths unlock 1.1% insurance yields, compounding with main bet advantages.

But here's where it gets interesting: puzzles like the "insurance correlation" trap novices, who insure on every ace regardless of count, surrendering 7% edges while missing +EV spots; case studies from tournament pros reveal selective insurance as a chip accumulator, with one tracked player gaining 18% edge in heads-up finals by betting only at +5 true. Observers point out how team play amplifies this, signaling big insurance lays to signal ten-rich shoes for partners.

Now, as of March 2026, updated simulations incorporating AI-driven shoe modeling from EU research labs indicate that online live dealer insurance—streamed from Malta studios—yields 7.1% edges under 65% pens, but hybrid RNG-physical hybrids introduce exploitable biases detectable via pattern software.

Common Probability Puzzles and Misconceptions

Insurance puzzles abound, starting with the myth that past blackjacks predict future ones, yet independence holds per hand absent counting; players chasing "due" dealer tens insure blindly, inflating losses by 9% in variance-heavy decks. Another head-scratcher: why 2:1 payouts don't break even despite 4/13 odds, a non-transitive quirk where vig hides in the math, much like sports book juice.

Studies found that grouping insurance with side bets compounds edges to 10%+ total, as seen in player logs where combo abusers bust 25% faster; conversely, abstainers preserve bankroll variance for main bet swings. It's noteworthy that surrender options pre-insurance check mitigate ace vulnerabilities better, shaving 0.3% edges without side wagers.

Take one analyst who modeled 10 million hands: insurance resolution times averaged 12 seconds per ace, slowing table pace and indirectly boosting house rake via hands per hour; this temporal cost, often overlooked, adds 0.1-0.2% effective edges in crowded pits.

Conclusion

Data consistently shows blackjack insurance as a negative-expectation play for non-counters, with 7%+ edges grinding down casual bankrolls across formats, yet selective application unlocks edges for the skilled amid finite deck puzzles. Players tracking patterns via apps or logs uncover payout rhythms tied to composition, avoiding traps like even-money folds or streak chasing; as March 2026 brings refined online tracking tools, those decoding probabilities stand to minimize drags while maximizing rare upsides. Ultimately, understanding these mechanics empowers informed skips over impulsive bets, aligning sessions with sustainable math over momentary lures.